Central bank policy interest rates don't have a macroeconomic rationale - Sink in the crisis or look for alternative monetary instruments? Part I 🙏

The purpose of this article is to highlight the urgent need to critically review the macroeconomic rationale of monetary policy model of Sri Lanka which confronts a severe macroeconomic and social crisis driven by foreign currency and debt, despite the sovereign monetary and central banking system. Given the technical nature of the subject, this article contains a series with the part I presented today.

Input for thought from Argentina

On August 14, the

Central Bank of Argentina raised it policy rate by 21% to 118%. This has been

the policy response to the money market volatility created by a sweeping policy statement made by the front running, far-right libertarian Presidential candidate Javier Milei who won the primary election.

His statement was that, if he won the election, he would close down the central bank and dollarize the economy with free banking.

His reasoning is as follows. There is no demand for the local currency where the demand is for the dollar. Therefore, the local currency should be at zero price, but the central bank manipulates the price and makes seigniorage profit which is more or less a swindle by politicians against the good people. One of the greatest thieves of the mankind is the central bank. He claims that the present inflation around 113% and expected of 141% by end of December can be resolved only by the dollarization.

The policy response was the devaluation of currency by 18% linked to policy interest rate raised by 21% to 118%. One cannot imagine how a modern monetary economy and living standards can operate and survive at policy interest rates and inflation rates at such sugar high levels and underlying business risks confronted by markets. There is no doubt that the monetary side of the economies in countries with unbearably high interest rates and inflation rates and central bank looking after the monetary economy have either failed or do not serve the general public.

Argentina despite its rich natural resources base inclusive of gold, gas and petroleum is a defaulted country since 2002 now struggling in poverty at a rate of 40% caused by the failure of the country's macroeconomic governance system. All IMF programmes that normally prescribe fiscal and monetary controls have failed with the latest offer of US$ 44 bn to service IMF's own loans. The Government is largely funded by the central bank.

As such, Argentina runs a two-decade long economic crisis despite the central bank being responsible for economic, price and financial stability like in all other countries. Therefore, the statement made by the Presidential candidate Javier Milei seems to have a strong macroeconomic ground to countries such as Sri Lanka.

Two main reasons are; First, they have confronted bankruptcy by running on foreign currencies despite the existence of the central bank to protect and promote economy with sovereign currency. Second, the monetary policy is built on policy interest rates and monetary financing.

Therefore, economic crises confronted by these countries have primary sources to flawed monetary policies adopted in violation of macroeconomic principles and central bank public mandates on regulation of sovereign currencies for the stability of the economy.

Prevalence of real economy and monetary economy - The central bank's role

Unlike in barter-based primitive economies, modern monetary economies operate through markets that run on transactions of money. Therefore, each economic transaction is an exchange between real resource and monetary resource. As such, any economy is a combination of real economy and monetary economy where real economic activities and monetary economic activities are inter-connected and inter-dependent on functions of money as a unit of account/value, a medium of exchange, a liquid store of wealth/value and a medium of deferred payments.

Given the role of money in modern monetary economies, money is a public good legalized under laws of land with sovereign powers vested with the central banks and other state regulators. Therefore, it is the government that is eventually responsible for a fair access to and distribution of the role of money across the economy in the general public interest. In this regard, monetary policy assigned to central banks for regulation of money and monetary distribution (i.e., credit and banking) is of utmost importance for orderly functioning of economies.

However, the country literature across the globe reveals that any economic crisis is directly linked to problems of the monetary economy such as debt/credit and currency crises which are attributable to the lapses in the monetary policies. This position is common for all countries, irrespective of whether they are developed market economies such as the US and Europe or developing market economies such as Argentina and Sri Lanka.

It is in this context that this article investigates the macroeconomic inappropriateness of central bank policy interest rates being the key policy instrument globally used in monetary policies to drive monetary economies of respective economies.

Sri Lankan monetary policy model

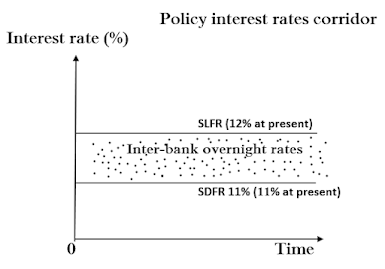

The policy model evolved from early 2000 on the technical assistance of the IMF and World Bank operates on the policy interest rates that set the target for the variability of overnight inter-bank interest rates. Policy interest rates at present are the standing deposit facility rate (SDFR) and standing lending facility rate (SLFR) which are the interest rates on overnight funding operations of the central bank with commercial banks.

The SDFR is the interest rate paid by the central bank on overnight deposits held with it by commercial banks. In contrast, the SLFR is the interest rate charged by the central bank on its overnight lending collateralized by government securities to commercial banks. The SDFR and SLFR at present is 11% and 12%.

These two rates are considered as policy interest rates corridor set for the variability of inter-bank overnight interest rates in the sense that no bank will need to borrow from or lend to any other bank outside this corridor as standing facilities at the central bank are financially more beneficial (see the chart below).

However, many central banks do not set such policy rates corridors but adopt policy rates as a general guide for overnight inter-bank interest rates and short-term interest rates along with other policy instruments inclusive of credit distribution-based refinance and balance sheet operations. Few instances are highlighted below.

- The US Fed announces the federal funds rate target range, 5.25%-5.50% at present, which is a hypothetical number. Therefore, the Fed uses several monetary instruments to ensure the the federal funds rate target range and to provide the economy with a variety of liquidity needs as follows.

- Interest rate paid on bank excess reserves (IOER) held at the Fed, i.e., 5.4% at present, to guide the inter-bank overnight interest rates (i.e., federal funds rates) within the target range.

- Open market operations to guide the inter-bank overnight interest rates (i.e., federal funds rates) and to control the yield curve, depending on the requirements of the economy.

- Primary credit rate (5.50% at present) up to 90 days, secondary credit rate (6.00% at present) very short-term mostly overnight, seasonal credit rate (5.40% at present) up to nine months and bank term lending rate (5.45%) up to one year on collateralized lending to banks and lending institutions to support the flow of credit to households and businesses

- The European Central Bank's (ECB) policy interest rates model has four layers, i.e., collateral based main refinancing rate weekly basis, overnight deposit facility rate below the main refinance rate, overnight marginal lending facility rate above the main refinance rate and the interest rate on statutory reserves (4.25%, 3.75%, 4.50 and 0%, respectively, at present). In addition, the ECB carries out targeted long-term refinancing operations and purchase of public and private securities as part of the monetary policy package to support the credit distribution.

- However, the Bank of England operates only the Bank Rate (5.25% at present) for overnight lending to banks and trade of government and corporate bonds (holding of 875 bn and 20 bn, respectively, at present).

- In the case of Central Bank of China, there is a set of benchmark/policy interest rates for short to medium-term based on refinancing together with statutory reserve ratios, open market operations and selective credit controls. The benchmark interest rates are overnight discount rate, rate of refinancing of secured loans, rate on temporary accommodations without collaterals for 10 days (1.875%, 2.25% and 4.125%, respectively, at present), one year loan prime rate (target for corporate loans) and five year loan prime rate (target for pricing of mortgages)(3.45% and 4.2%, respectively, at present). Therefore, Chinese monetary policy is widely a credit distribution policy and it accepts that effects of policy rates are not significant unless they are accompanied by other policy tools.

- Meanwhile, the monetary policy of Bank of Japan is based on overnight interest rate on current account balances held by banks (negative 0.10% at present), purchase of 10-year government bonds for a yield target around zero with a range of plus or minus 0.50% (yield curve control) and purchase of exchange traded funds up to 12 trillion yen, real investment trusts 180 bn yen, commercial papers up to 2 trillion yen and corporate bonds up to 3 trillion yen. As such, Japanese monetary policy is primarily conducted for targeting overnight inter-bank interest rate and government 10-year bond yield while providing a limited liquidity to corporate finance/credit markets. It is noted that the monetary policy has been ultra loose during the past two decades due to deflationary crisis confronted by Japanese economy.

However, Sri Lankan monetary policy is essentially an overnight bank liquidity management support policy while letting the economy's credit distribution to banks and shadow banks based on their risk-taking decisions. Therefore, the authorities have to be mindful of whether this is the monetary policy the country requires at this juncture to navigate from the economic crisis and bankruptcy.

Primary monetary policy decision

The primary monetary policy decision taken from time to time by central banks in most countries is on the level of the policy interest rates, a cut or a hike or unchanged. The decision is taken to support their inflation control at annual targets, i.e., 4%-6% in Sri Lanka and India and 2% in developed countries, in the medium to long-term (timeframe now defined).

The underlying macroeconomic justification for any change in policy interest rates is as as follows.

- Inter-bank interest rates and money market interest rates including government securities yield rates change quickly.

- Bank interest rates change.

- All other interest rates in organized and unorganized credit markets change.

- Credit expansion changes, i.e., tight credit conditions or relaxed credit conditions, in response to changes in interest rates.

- Change in credit conditions affect the aggregate demand, i.e., consumption and investment, in the economy. This mean that tight credit conditions slow down the aggregate demand and vise versa.

- The change in the aggregate demand affects the general price level or its change (inflation). This mean that lower aggregate demand reduces inflation or growth of general price levels and vise versa.

For example, the Bank of England has been in the hiking cycle from December 2021 by raising the policy interest rate from 0.10% to 5.25% so far while inflation rose from 5.1% in November 2021 to 11.1% in October 2022 and has now slowly moderated to 6.8% in July 2023 after 19 months of policy rate hike cycle. Another hike of 0.25% in next month is the market forecast, given still red hot inflation. The high inflation or the cost of living problem in the UK is the new from of financial crisis confronted by the general public although the Bank of England has the independent mandate of maintaining the price stability.

Accordingly, the present form of monetary policy model is to raise policy interest rates during periods of inflation rising above the target and to cut rates when the economy confronts lower inflation or recessionary periods. For example, central banks in developed countries kept policy interest rates around zero and negative levels for about a decade to fight the recession caused by the global financial crisis 2007/09.

All monetary policy decisions are highly judgmental, despite they are being called data dependent, and grave policy mistakes that have caused significant instabilities of economies are well documented. One case in point is the faster rate hike cycle pursued by the US Fed in 2017-2018 (i.e.. from 0.50%-0.75% in December 2016 to 2.25%-2.50% in December 2018, i.e., 8 consecutive hikes of each 0.25%) due to flawed forecast of inflation where the Fed had to give up and reverse the cycle forthwith by publicly accepting it as a policy mistake.

Therefore, policy interest rate is not a God-given macroeconomic weapon to attack all corners of the economy to drive it towards the wishes of central banks because economies are driven by a system of active markets that do not operate under the bureaucratic command of the central banks.

Macroeconomic inappropriateness of policy interest rates

The evidence in this regard is diverse. The most important evidence is the non-risk-taking in credit transactions at policy interest rates, despite the fundamental fact in credit is the risk-taking.

Therefore, this part of the article focusses only on macroeconomic inappropriateness of policy interest rates in the context of non-risk-taking on central bank credit operations. The technical evidence is provided under three items below.

1. Interest rate as the price for risk-taking

Any credit transaction is a combination of functions of money as a liquid store of wealth and a medium of deferred payments that involves risks to both the lender and the borrower.

The lender sacrifices the present utilization of monetary wealth (purchasing power) to utilization it in future. Therefore, the lender faces an opportunity cost in lending and charges a monetary fee to cover the cost. The borrower has the opportunity to utilize money at present and earn a return or benefit through the advanced use of money and is prepared to pay for it.

However, both the lender and the borrower face risks on the money during the credit period. The risk has two components, the real business risk and inflation risk. This risk concept can be modelled by the Fisher Equation used in economics as presented below from the point of view of a lender.

- Real interest rate = Agreed (monetary) interest rate - Expected increase in the general price level (inflation) during the credit period

This states that the real return the lender is willing to receive from lending is the difference between the agreed interest rate on the loan and inflation expected during the loan period. The expected inflation is subtracted to estimate the actual interest rate because inflation is a loss of the purchasing power of money lent during the credit period.

However, this concept does not look at how lenders determine the monetary interest rates. Therefore, this equation is adjusted to explore how lenders determine monetary interest rates by considering risks underlying the business of lending of money.

- Agreed (monetary) interest rate = Real interest rate + Expected inflation

In this concept, real business risk and inflation risks are the two components in determination of interest rates on money given in loans.

As lending is a business, a lender expects a real return adequate to cover his/her business risk. This includes risk of default attributable to the borrower and the economy in general. The borrower specific risk arises from personal characteristics and his/her business profile. Securities/collaterals taken from the borrowers are only a source or instrument of mitigation of the loss in the event of risks realized.

The economy specific risks arise from the macroeconomic stability/instability. In countries like Sri Lanka which confronts a debt and currency crisis, macroeconomic risk involved in any economy activity is higher than in normal times. In such periods, as the trust in credit and money is generally affected, the risk equation is generally elevated on all parties. Therefore, governments give the priority to maintain economic stability in order to reduce the macroeconomic risk and its premium accounted in interest rates. This is the reason why market interest rates tend to rise when macroeconomic uncertainties are felt by the public and markets.

Globally, inflation risk has been historically higher since the beginning of 2021. Interest rates in high inflation countries such as Argentina and Zimbabwe are exorbitantly higher due to this inflation risk factor.

Accordingly, this equation shows that a lender charges a rate of interest based on real return expected to cover risks to him/her on real business plus a premium to cover the expected risks on purchasing power of money lent during the credit period. However, the technical issue is how to measure the two risk categories based on real world data to determine the interest rate in numerical or monetary values as there is no standard mathematics to measure such future outcomes.

Sophisticated lenders such as global banks resort to various credit risk rating models to measure the real business risk. The expected inflation is mostly estimated through the time series of monthly consumer price indices released by the state statistical authorities. However, village money lenders who do not have such technical data also determine interest rates based on own informal knowledge in businesses around them.

In determination of bank interest rates, regulatory limitations on banking business operations such as statutory reserves, capital, liquidity, asset classifications and impairment charges also add to cost of funds and are priced in bank interest rates.

Therefore, there is a wide range of interest rates in credit markets (formal and informal) based on risk assessment of respective credit transactions. It is general practice to compare interest rates to understand differences in risks across credit transactions. A rule of thumb is that interest rate rises with risks, i.e., the higher the risk, the higher is the interest rate.

Credit granted to governments carries lower interest rates as governments can service loans by the rollovers of credit through the creation of new money unlike in private business credit. Banks offer lower interest rates on credit to large business corporates than to SMEs due to lower business risks of corporates. Pyramid investment operators offer exorbitant rates of return to subscribers as the operators know the high risks taken on such investments. High interest rates charged by village or informal sector lenders on daily or monthly basis are well known for the magnitude of risks they take.

However, the interest rate concept pursued by Islamic principles prohibits pre-determined rates based on pre-risk assessment shown above. Accordingly, Islamic principle is the profit-loss sharing rate agreed on utilization of loan funds. Therefore, the difference between Islamic principle and standard finance principle is not on the risk-taking but on how the return on risk-taking is distributed between the lender and borrower.

2. No risks involved in policy interest rates

Central bank credit operations do not confront business risks highlighted above due to several reasons.

- The central bank prints money for credit operations without any external cost of funds.

- Its customers are the banks tightly regulated and supervised by itself.

- Its credit operations are overnight and very short-term liquidity operations where banks operate settlement and reserve accounts with the central bank.

- Its lending is fully collateralized by high quality securities.

- Its deposit operations are only book entries of liabilities between currency and reserve deposits over money already printed. Therefore, there is no any risk of repayment of overnight deposits to banks.

- Due to very short-term nature of credit of the monetary authority, the central bank does not confront inflation risk. As the control of inflation is the mandate or objective of the monetary policy, it is not ethical for the central bank to charge a premium on its inflation forecast or target.

Further, inter-bank lending involves risk-taking as banks confronts business liquidity risks on a daily basis and such lending is not collateralized. As such, banks with weak financial conditions are unable to borrow from the inter-bank market. Therefore, the use of risk free policy interest rates corridor to target the variability of risky inter-bank interest rates is flawed in both economics and finance.

Interest rates applied on open market operations also do not have a risk basis as revealed from actual rates. In open market operations, the central bank carries on lending (reverse repos) and borrowing (repos) to regulate the liquidity of the banking system primarily to drive inter-bank overnight interest rates at or around certain points within the policy rates corridor as preferred by the central bank. Therefore, this interest rate point is another policy interest rate not announced or disclosed by the central bank.

Due to the ad-hoc, bureaucratic nature of open market operations, overnight and term reverse repo rates often are reported to be lower than the SLFR while the opposite holds for repos (repo rates are higher than the SDFR). For example, today (22 August), the central bank provided Rs. 94.1 bn of overnight reverse repo funds at interest rates between 11.40%-11.80% which are lower than the SLFR of 12%. It is hard to understand why even term repos are offered at interest rates lower than the SLFR. This has been the regular practice in open market operations in the recent past.

The determination of repo and reverse repo rates in this manner inconsistent with standard policy interest rates does not have an economic rationale other than providing financial benefits to selected money dealers. In certain times, the central bank carries on open market operations to control certain points/segments of the so called yield curve without any transparency. Therefore, such repo and reverse repo rates have become another layer of unjustified and undisclosed policy interest rates used in the monetary policy.

3. Inability of policy interest rates to influence or intervene in risks involved in private credit

It is clear that credit flows in the economy involve a wide range of risks and, therefore, interest rates as prices for underlying risks. In this context, changes in risk free policy interest rates announced in the monetary policy cannot be expected to change the risk profiles of credit flows in the economy that are determined by credit markets. Therefore, the fundamental fact is clear that policy interest rates being risk free do not have any elements to influence real risk premium and inflation premium priced in market interest rates. Therefore, credit flows cannot be expected to change in response to changes in policy interest rates as central banks state in their theoretically drafted media statements.

This is reason why some central banks are accustomed to advise or threaten banks with administrative/regulatory actions unless banks revise their interest rates in line with policy interest rates. For this purpose, central banks resort to their prudential regulatory and supervisory mandates as present monetary policy models do not recognize such direct credit controls (with China as an exception). Therefore, such administrative interventions in bank credit operations or credit markets are inconsistent with the market-based macroeconomic principles believed in policy interest rates based monetary policy models. This is the position for the Sri Lankan central bank too.

However, some central banks are empowered with risk-sharing policy instruments in respect of credit flows to identified sectors/activities. Refinance and credit guarantees are two such monetary policy instruments. Even the US Fed and European Central Bank extensively use refinance (discount window) to help credit flows across households and businesses. Deposit insurance also is a credit risk sharing instrument helping the wider financial intermediation.

Although Sri Lankan central bank extensively used such risk sharing instruments in the past to promote credit/financial inclusion, the new legislation has repealed those provisions. Therefore, the central bank at present does not have any policy instruments for promotion of financial inclusion or fair distribution of credit and monetary resources across the priority sectors and activities. This raises a grave concern over the ability of the Sri Lankan monetary policy to navigate the economy from the present crisis and bankruptcy.

Many central banks eased bank credit regulations such as statutory reserves, capital adequacy, liquidity, non-performing loan classifications and loan loss provisions as part of ultra relaxed monetary policies that were followed in 2020/21 to help banks reduce interest rates and promote credit to fight the global corona pandemic-induced economic disruptions. Such credit regulations also raise costs of funds on banking business operations which are passed on to interest rates. However, changes in policy interest rates do not affect the component of bank interest rates attributable to such banking regulations.

Interim Concluding Remarks

This article reveals following key points.

- Sri Lankan policy interest rates are risk free rates.

- Therefore, monetary policy decisions and implementation based on policy interest rates cannot affect interest rates and the flow of credit in the economy as conceptualized in monetary policy transmission mechanism.

- The non-availability of credit risk sharing and credit distribution instruments is the fundamental lapse in Sri Lankan monetary policy when compared to many countries including developed countries.

- Therefore, there is no macroeconomic rationale for the present Sri Lankan monetary policy model to maintain or promote the stability of the economy.

- The monetary policy proposed under the new central bank legislation will be a disaster to the sovereign monetary system.

- Therefore, the way forward should be for the central bank to redesign the monetary policy with risk-taking credit and interest rates with a focus on credit distribution across the priority sectors and activities.

- Otherwise, risk free policy interest rates and overnight bank liquidity management support-based monetary policy model that always makes seigniorage profit will only be a swindle against the general public unless policy interest rates are kept around zero to reflect the zero risk exposure. In any context, the price stability objective story or inflation control at a target will only be a bluff. This is why the Presidential candidate of Argentina proposes to shut down the central bank by labelling it as one of the greatest thieves of the mankind as it does not serve the monetary side of the economy.

(To be continued)

(This article is released in the interest of participating in the professional dialogue to find out solutions to present economic crisis confronted by the general public consequent to the global Corona pandemic, subsequent economic disruptions and shocks both local and global and policy failures.)

P Samarasiri

Former Deputy Governor, Central Bank of Sri Lanka

Comments

Post a Comment