CB's new macroprudential - A rocket science for preventing bank runs? or Another bureaucratic profession of no benefit to the public?

Article's Background

The Central Bank (CB) released a 12-paged pamphlet on "Macroprudential Policy Framework" on 14 March 2024 (see the press release)(see Pamphlet).

- According to its contents, the pamphlet spells out the policy framework that will be used to secure the CB's statutory object of financial system stability as set out in the section 6 of the Central Bank of Sri Lanka Act, No. 16 of 2023.

- Therefore, the framework is to comply with the macroprudential authority in Sri Lanka vested with the CB as stipulated in the Part X of the Central Bank Act which provides for relevant macroprudential objectives, powers and instruments.

- relevant macroprudential professionals of the CB have no idea of macroprudential concept that has already failed in the world as well as in Sri Lanka and

- therefore, this macroprudential policy framework referred to in the CB's pamphlet and the Act will be nothing bust another unproductive bureaucratic line of professionals in the CB.

In modern monetary economies, the structure of the system that distributes money across the society through various financial products is the key to decide the phase of development and living standards. Unlike in other businesses, financial businesses are heavily regulated by the government, given their inherent risks. Therefore, the key message of the article is this. Regulators must be honest in regulating the system and disclosing information to ensure the safety and soundness of the system largely through the market discipline while facilitating the development and outreach of financial products to finance the real economy and living standards across all corners of the society. Otherwise, all hypotheses of all bureaucratic lines and elected governments will serve no purpose to modern stage of human development.

Macroprudential means the approach of banking regulation designed to deal with risks identified from business trends of sector/industry aggregates. Banking implies conventional commercial banks as well as shadow banks, i.e., non-banking financial firms that are engaged in banking-like businesses.

How this approach is implemented involves in a lot of fancy hypotheses and terms. In general, this approach is focused on tracing of so called "systemic risks" that are developing across the banking sector.

Systemic risks are the undesirable possibilities that can cause sector-wide bank runs and failures, the situation known as the lack of funds to repay bank depositors/customers. This can happen in one bank and spread to several banks in a shorter period.

The banking business is such that it can grant loans though book entries by creating deposits in bank books. Banks manage this business by holding little cash at hand while cash deficits are managed through very short-term borrowing from the money market including the central bank. Therefore, banks are inherent in facing shortfalls of funds to meet their payments, mainly withdrawal of deposits and release of loans.

Therefore, a bank run is essentially the result of poor or fraudulent management of finance of a bank. The financial fraud means the inappropriate management of bank finance and internal operations without regard to cash deficits inherent in banking business. Therefore, the generic risk confronted in banking business is the fraud. All fancy terms of banking risks such as liquidity risk, credit risk, market risk, interest rate risk and operational risks are accounting-based descriptions of unfavorable outcomes of the generic banking risk.

The systemic risk in macroprudential is interpreted as the outcome or result of business concentrations, inter-connectedness and fragile herd behaviour of general public trust in banking. Therefore, macroprudential framework is said to be implemented to mitigate such outcomes that cause systemic risk. However, there is no any such risk type by the name of systemic risk identified from accounting or financial concepts. Therefore, systemic risk is the worst outcome confronted by banks due to generic banking risk of fraud.

What is micro-prudential?

It is the conventional approach or system of bank regulation carried out over each bank to ensure that each and every bank operates in safe and sound manner to protect customer trust in banks. Therefore, the generic of bank regulation is to discipline banks against fraud. Accordingly, the regulatory system contains three broad categories of actions.

- Licensing and issuance of rules or a code of business conduct to limit business risks to prudent levels.

- Examinations of business operations to assess the level of safety and soundness or condition of affairs whether a bank is able to meet its financial obligations or continuation of its business is likely to involve losses to depositors and creditors.

- Resolution of problem banks including provision of safety net action (lender of last resort and compensation of deposits), business restrictions, reconstitution of management, restructuring and winding up in a manner to prevent runs on banks.

In that context, systemic risk is inbuilt in generic bank regulation where bank regulators examine the extent of inter-connectedness, concentrations and financial conditions of each and every bank. Therefore, the macroprudential is only a tool of bank regulation. However, the resolution of any systemic concerns needs tools of conventional bank regulation or micro-prudential framework.

Origin of macroprudential hypothesis

The origin of macroprudential terminology and approach is the banking in developed countries exposed to asset bubbles connected with business cycles (booms and downturns) through financing of assets by bank credit. Assets are stocks, bonds, derivatives, property and investments.

The business boom helps asset bubbles, i.e., rising demand an prices, where the downturn causes bubble burst in the event the bubble is too big and unhealthy. Therefore, a bubble burst is likely to cause banking crises unexpectedly as it erodes bank assets and funds. In this context, bubble burst is considered as the trigger point of systemic risk. The last global financial crisis of 2007/09 is considered as a similar asset bubble burst. All banking crises in the past in developed countries are connected with such asset bubbles behaviour.

The macroprudential terminology emerged immediately after the last global financial crisis in the US and Europe to replace the financial stability terminology that was popular until then. Almost all countries had financial stability frameworks under same hypothesis of detecting and mitigating systemic risks which miserably failed in 2007.

Origin of financial stability hypothesis

This emerged in the UK in 1997 with the adoption of consolidated supervision approach for the financial system. Consolidated supervision means the integration of regulators to supervise all financial sectors, i.e., banking, insurance and securities trade/investment banking, under one roof so that risks that cut across all financial businesses/sectors are handled by a single regulator as against a conventional system of multiple or divided regulators that operates with different mandates, approaches and locations.

Accordingly, the UK regulatory system was reformed in 1997 to create three layers.

- Consolidated supervision - bank regulation was taken out from the Bank of England and vested with the Financial Supervisory Authority (FSA) as the single regulator for all financial areas.

- Independent monetary policy - the Bank of England to conduct the monetary policy for inflation target given by the government free from bank regulation-connected biases.

- Financial stability - the Bank of England to monitor build-up of asset bubbles independently under a three partite financial stability committee, Bank of England, Treasury and FSA.

The whole framework miserably failed in 2007 when Northern Rock bank suddenly confronted a country-wide run in October 2007.

- Neither single regulator FSA nor the financial stability framework could stop the run spreading over the financial system. The Bank of England declined to provide lender of last resort to the Northern Rock at the beginning of the run due to the confusion of responsibilities but, while the run was spreading, it bailed out Norther Rock as usual to contain the contagion. However, the system was saved later by nationalizing all banks as the stability framework miserably failed.

- Under the post-financial crisis reforms in 2010, the prudential regulation of banks and financial institutions was given back to the Bank of England with a new entity of Prudential Regulatory Authority (PRA) while the consumer protection of financial firms was entrusted with the FSA which was reconstituted as the Financial Conduct Authority (FCA). In the Bank of England, Financial Policy Committee (FPC) was set up for making policy decisions to promote the resilience or stability of the UK financial system parallel to the Monetary Policy Committee (MPC) responsible for Bank of England interest rate decisions. The MPC has the power to issue policy directions to both PRA and FCA.

In contrast, the US followed the conventional multiple regulator system comprising of a large number of sectoral national and state regulators without any specific financial stability framework. Despite the multiple regulatory system, the financial crisis 2007/09 originated in the US and worst hit there.

- However, after the global financial crisis, the US government accepted the financial stability concept and set up the Financial Stability Oversight Council (FSOC) in 2010 under the Dodd-Franck Act. It is chaired by the Treasury Secretary participated by other line regulators such as Fed, Federal Deposit Insurance Cooperation (FDIC) and Office of the Comptroller of Currency (OCC). However, FSOC has no enforcement powers other than periodical meetings and the release of research reports and annual reports.

- However, with all these multiple bank regulators and FSOC, the US confronted a severe banking distress in March 2023 suddenly with a failure of three mid-size banks without any early warning detected by any regulator including the Fed. The distress was urgently resolved by opening of the emergency lending facility (LOLR) by the Fed where nearly US$ 300 bn were used in just one week to keep the general public trust in the banking system. This is the old fashion LOLR which has nothing to do with modern fancy tools of financial stability or macroprudential hypotheses.

Origin of financial stability hypothesis in Sri Lanka

This took place through several new initiatives taken in the CB.

The first step was the work on public awareness to make the public aware of the financial system and financial services, risks and nature of regulations on the guidance of Governor A S Jayawardena beginning 2001.

- Two-Page Paper Supplement titled “A Guide to

Financial Services in

- One page paper advertisement on “A Guide to Interest Rates and Fees of Banks”, May 2003 (Sinhala, English and Tamil)

- Paper Advertisement on “Institutions Legally Permitted to Accept Deposits from the Public”, (Sinhala, English and Tamil) – published since September, 2002 periodically

- "It should be clearly understood that there are risks to be borne by depositors and borrowers of any financial institution whether it is a bank or a finance company or any other. The return on a deposit or the cost of a borrowing or a transaction with a financial institution will reflect the degree of risk, among other things. The fact that certain financial institutions are supervised or approved by the Central Bank does not involve a guarantee of deposits, loans or transaction of public with those institutions, whatsoever. The Central Bank, however, regulates and supervises the institutions to encourage them to act in a prudent manner, which will eventually protect the public interest."

- "However, there is a certain misconception that, as supervisor and regulator, the Central Bank guarantees the safety of all public deposits. While the regulators seek to achieve the safety and soundness of the financial institutions regulated by them, yet the safety and soundness of the institutions depend largely on the management of the institutions by their directors and managers. Therefore, it is the responsibility of depositors to exercise due care and vigilance on the financial institutions when placing deposits."

This is the first time in the history that the CB told the public the blunt truth on risks and return on finance without any guarantee from the CB.

The second step was the attempt to financial stability-based reforms to financial sector regulation on the influence of the World Bank and IMF. Some of them known to me are listed below.

- In line with the UK model, by 2000, an industry committee chaired by the CB Governor had agreed with a proposal to set up a UK style FSA by merging regulatory works of the CB, SEC and IRA. The recommendation was to amalgamate SEC and IRA first and combine the CB at the next stage. In that line, another attempt was made in 2004 to set up a FSA inclusive of regulatory arms of the CB. Based on objections raised in the report I submitted to the Monetary Board and Treasury, the CB was taken out from the FSA model which was still born. If that model had operated, Seylan Bank crisis in 2008 would have been another Northern Rock event.

- In 2002, FSA and financial stability framework in line with the UK model were attempted by the World Bank/IMF under their FSAP (Financial Sector Assessment Programme) and central bank modernization project for Sri Lanka.

- In November 2003, Financial Stability Committee (FSC) was set up in the CB. The FSC was chaired by a Deputy Governor and comprised heads of financial sector connected Departments. I was the Secretary to the (FSC). Therefore, I drafted the TOR of the FSC as follows. The FSC was assisted by a Study Group drawn from regulatory Departments.

- assessing the risks and vulnerabilities leading to major instabilities in the financial system in the foreseeable future,

- monitoring the financial system stability and submitting periodic reports to the Governor and the Monetary Board, recommending policies necessary to promote the financial system stability and

- preparing Financial Stability Report (FSR) periodically.

- The FSC set up a Study Group drawn from relevant Departments to compile Financial Stability Indicators and reports including Financial Stability Review released in 2004 and 2005.

- Based on a recommendation by the FSC, a Working Group was set up in September 2005 to study financial conglomerates and propose regulatory measures to prevent systemic issues. At that time, it was believed that the very source of systemic risk or financial instability was the operation of financial conglomerates. However, only report it drafted was on the status of financial conglomerates in Sri Lanka which did not have any practical application.

- In June 2006, it was decided to set up a Financial Stability Unit in the Bank Supervision Department to cater to FSC as an interim arrangement until a a dedicated Financial Stability Department was set up later. However, the Stability Unit did not materialize.

- Two publications were released in 2005, the pamphlet on Financial System Stability (read it here) and Financial System Stability Review 2004 (not available in the CB website), under the supervision of the FSC. The first drafts of the pamphlet and financial system of part of the Financial System Stability Review 2004 were compiled by me. All together, 7 pamphlets were issued.

- In January 2007, Inter-regulatory Institutions Council (IRIC) chaired by the Governor was set up to coordinate the assessment of systemic risks based on views deliberated by the members. I was a member in the capacity of the Director of Bank Supervision.

- As the IRIC was not operational as expected other than few meetings of industry friends, I reconstituted it in early 2015 as Financial System Oversight Council (FSOC) in line with US FSOC but it also was not operational other than few meetings. The new Central Bank Act has recognized it in the Part XI as a statutory body to cooperate in systemic risk and macroprudential policy. However, it does not have any mandate to deal with systemic risk issues other than meetings, discussions and information sharing.

Further experiment of financial stability subject by the CB

The experiment is a complete failure as highlighted below.

- In January 2007, a separate Financial System Stability Department (FSSD) was set up in the CB. Later, on my proposal, the name of the FSSD was changed to Financial Stability Studies Department in November 2011. The complaint was the misinterpretation of the financial stability of the country as being maintained by this particular isolated Department although it in fact was secured by bank supervision and other regulatory departments.

- Its name was again changed in November 2014 as Financial Sector Research Department (FSRD) as no contribution was received from the Department. Later in 2017 it has been renamed as Macroprudential Surveillance Department (MSD) to give a fancy outlook to this dormant department. The latest attempt is the macroprudential authority provided for in the new Central Bank Act.

All reports and meetings handled by the stability framework were meaningless works that satisfied only those who drafted them. This was another department to post unwanted staff members. Therefore, name change of three times was like the change of pillow for the headache.

After I left the stability subject in the latter part of 2006 take charge as Director of Bank Supervision, I never associated with the specific stability work as I knew its uselessness in the prevailing model in the world. When I became the Chair of the FSC by office of Deputy Governor, I declined to convene meetings and informed the Governor that I would not involve in the work, given fundamental reasons. As a result, another Deputy Governor who liked meetings and reports received the FSC Chair post.

I give two instances below to highlight that this Department did not have a focused line of research from the inception.

- I recall at a meeting of the senior management of the CB chaired by the Governor, then Head of the Financial Sector Research Department who is now a Deputy Governor made a conclusion after making a colorful presentation that the financial stability prevailed in the last quarter. I immediately responded that "you don't have to say it because we know it as nothing of that sort happened in the last quarter." Then, the Governor advised her that her duty was to communicate early warnings of any major instabilities detected by the research of the Department.

- Meantime, I arranged a quarterly macroprudential assessment report from the Bank Supervision to the Monetary Board based on selected timeseries of aggregate banking statistics. Financial Sector Research Department also had an ad-hoc habit of submitting fancy Board papers on subjects the Head preferred. I remember one paper stating a finding that the suspension of private bond placement system had caused inflationary pressures. The reason given was the subscription of the CB to Treasury bill auctions to control yield/interest rates as there was no backup funding of private placement system to raise funds outside the market and the resulting increase in consumption in the economy through such money printing.

- However, inflation analysis and control was not the mandate of this Department. At that point, the CB holdings of Treasury bills was around Rs. 200 bn with inflation around around 4%. If that view holds true, the increase of Treasury bill holding of the CB to Rs. 2.7 trillion in the recent past would have collapsed the currency system by now similar to Zimbabwe due to galloping inflation. This Head was the Superintendent of Public Debt earlier who abused the private placement system. Therefore, he wanted to reintroduce the system to justify the system.

This Department had few sidelined staff members who never had any regulatory and supervisory experience. What they did was to prepare colorful reports and power-point presentations to explain trends of financial sector statistics collected from other regulatory departments and stock market and to coordinate the Chapter 7 of the CB Annual Report.

Its reports were based on a large number of financial stability indicators compiled from information collected from other regulatory Departments and institutions. All such indicators are industry or sector averages or aggregates which are meaningless statistics. These indicators are biased toward the financial position of few large institutions and, therefore, do not reflect the actual for the most of institutions which follow different business models. Most indicators are based on complicated regulatory and accounting definitions that are not understood by relevant staff of the Department.

In fact, these indicators have no relevance to systemic risk sources such as interconnectedness and concentrations that is the very purpose of the stability assessments. Those who are interested in knowing what these magic indicators are can see them in the Appendix tables of the CB Annual Report. The major weakness of the stability reports drafted from these indicators was the inability to present the underlying story of emerging risks, micro-prudential or macro-prudential, other than highlighting trends and patterns of statistics with magical charts. This weakness is same for the Global Financial Stability Report of the IMF too. This is the general weakness of gall reports of the CB. Either the underlying story is not evident or the story is not supported from data. The overall weakness of the stability framework highlighted above is justified by two major risk events.

- With all these fancy FSC, Stability Reports, FSSD and Working Group, the country confronted the second finance company crisis 2008 through a few financial groups led by the Ceylinco Group which were concentrated in unauthorized shadow banking parallel to global financial crisis 2007/09. It had contagion effects on Seylan Bank, a systemically important bank, which was resolved through bank regulation powers.

- The country confronted the present debt and currency crisis in 2022 despite the fancy financial stability/macroprudential surveillance framework implemented implemented since 2017.

Unresolvable issues in the proposed macroprudential policy framework in Sri Lanka

What is presented in the CB pamphlet is nothing but the failed concept of financial stability framework outlined as above. All contents of the pamphlet are a bunch of technical jargon used by beginners of the subject. Therefore, the pamphlet appears to be an attempt of relevant staff to learn what this concept is. A few observations are presented below.

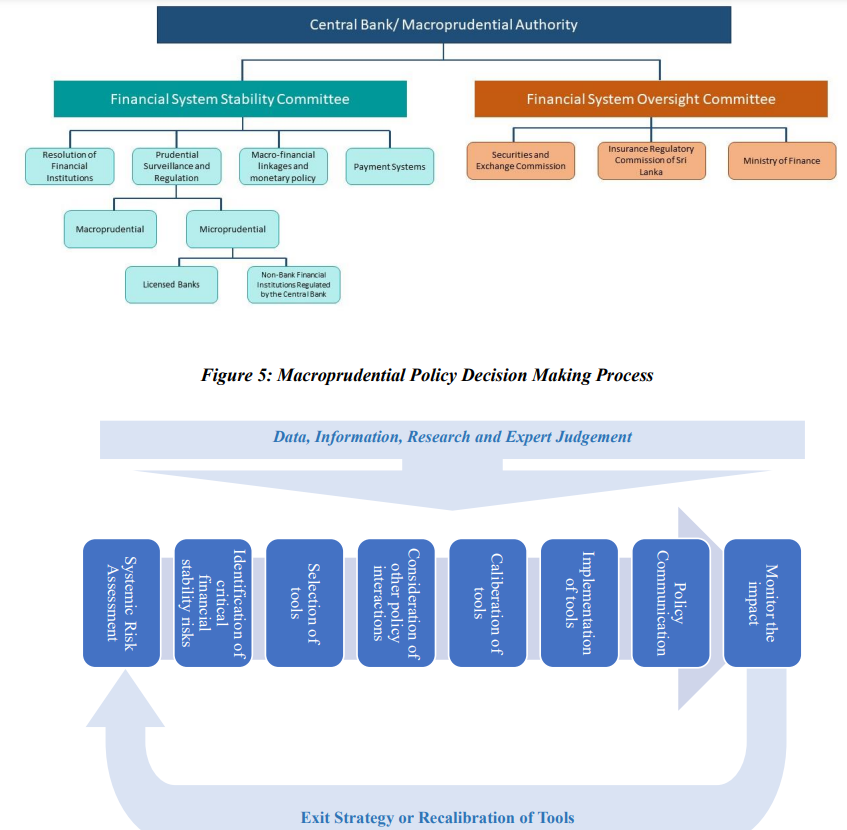

- First, the pamphlet presents the story of the policy framework in 5 diagrams as copied and pasted below that are not understood by even the pamphlet authors. Therefore, they think that the stated macroprudential framework is like a rocket science that can be presented on paper to secure the financial stability like pilots operate flights to destinations with greater certainty. Therefore, these diagrams are meaningless and non-operatable stuff.

- Second, macroprudential policies, systemic risk surveillance and indicators, macroprudential tools, interactions and institutional set-up and communication of macroprudential stance/systemic risk developments as stated in the pamphlet are only concepts that are not supported by practical applications in any country. In all countries, macroprudential/stability works are only another conceptual line of economic and financial research which has miserably failed so far.

- Third, three intermediate macroprudential objectives stated are fictitious objectives as they are not measurable and assessable with performance benchmarks. They are stipulated in the Central Bank Act too without any descriptions and interpretations of relevant terms. Even though those objectives are achieved on specific interpretations, there is no guarantee that financial crises will not touch down. No country has so far detected any real early warnings of financial crises from such objectives and assessments until they really hit. Further, the CB authorities do not provide any formal assurance that the country will never face any financial or banking crisis phenomenon because of this newly ambitious policy framework.

- Fourth, no regulators can prevent systemic risks or banking crises as there are no tools to curb financial fraud or control inter-connectedness, concentrations and public distrust of banks or financial firms from time to time as they are not measurable, traceable and monitorable on a daily basis. Further, those are determined to a large extent by the structure of the real economy and bank governance systems. Therefore, the best practice followed by most regulatory authorities is to keep the resolution system ready to recover the financial systems and economies without delay in the event of crises, rather than wasting time on assessment and prevention of unknown systemic risk triggers through such hypothetical and fancy frameworks of macro-prudence. The quickly opening up of the emergency lending scheme by the Fed in March 2023 to deal with the banking distress is a good example. However, the CB which talks about fancy framework of financial stability has abolished the conventional emergency lending scheme used to prevent banking/financial crises.

- Fifth, financial stability reports are only academic stuff useful for the survival of relevant research professionals as no body will understand systemic risks for their safeguards. In fact, regulatory authorities never divulge such risks to the public in advance even if they are detected by any luck, but make efforts to fix them covertly because any communication of such market sensitive risk information will immediately trigger crises.

- Sixth, the fancy concept of systemically important banks/institutions is meaningless because most financial crises in the past have originated from small institutions depending the the extent of customer trust affected. However, this concept stresses the need to monitor large banks closely in order to prevent systemic risk events. Last year, the bankruptcy of Credit Suisse, one of the two largest bank in Switzerland, did not cause any systemic bank runs and the bank was merged with the other largest bank, UBS.

- Seventh, bank regulation and financial stability/macroprudential hypothesis are founded on the myth of bank assets created on mobilization of short-term deposits. Therefore, they stress the need to protect depositor funds for the safety and soundness of banks and banking system. However, the truth is deposits are created by lending through book-entries where banks manage liquidity to cover the gap between cash outflows and inflows arising from bank assets and liabilities. Therefore, it is the protection of borrowers that will largely contribute to safety and soundness of banks and banking system.

- Eight, the general view of financial analysts is that the conduit for asset and credit bubbles that are behind systemic risks as presented by macroprudential experts is the arbitrary monetary policy cycles of central banks. It is believed that the global financial crisis 2007/09 was an asset bubble burst triggered by the monetary tightening cycle up to 2007 in the US and Europe. The monetary policy bureaucracy does not pay attention to bank balance sheets, cash flows and asset bubbles as they consider it as the responsibility of the line regulators, especially the macroprudential line. This is a result of foolish concepts presented two Fed Chairmen.

- First, Allen Greenspan - It is difficult to pick or prick asset bubbles. Therefore, it is better to allow bubbles to burst and then use the monetary policy/interest rate to repair assets.

- Second, Ben Bernanke - The use of interest rate to tame asset bubbles is like the use of sledgehammer for brain surgery.

- However, the monetary policy experts also don't have benchmarks to know the point of policy adequacy as they are driven by unmeasured concept of the monetary policy transmission mechanism. In addition, central banks in countries like Sri Lanka issue regulations on bank interest rates and reserve requirements to impalement the monetary policy through administrative measures and use bank regulation arm to enforce them without any regard to bank business models and requirements. This is unethical and unprofessional if monetary policy and bank regulation are considered independent each other. Therefore, the phase of the monetary policy cycle often ends up in asset bubbles and resulting bank problems. The current monetary tightening cycle that commenced in early 2022 in the world of central banks has caused an alarming degree of interest rate risks in both asset side and liability side of bank books world over. In fact, the turmoil confronted by banks in the US and Europe in March 2023 and now is considered as the direct result of monetary policy tightening/interest rates hiking cycle.

Food for thoughts to reconstitute and rebrand the system

- The Bank Supervision arm is the generic to ensure that the financial systems operate without major disruptions because banking information provides trends of all corners of the financial system and economic activities as they operate largely through transactions with banks.

- Therefore, what is most crucial is to use the Bank Supervision to ensure the discipline in bank governance and business lines with a futuristic view to contain the generic banking risk of financial fraud by prompt resolution of issues and concerns as and when they are found. It is really boils down to the view of the Head of Bank Supervision to what extent a bank is able to meet its payment obligations or is likely to default soon, which requires prompt resolution including LOLR.

- However, no bank can be made free from this risk, known as the liquidity risk, as banks operate in a fractional reserve system where the majority of deposit liabilities is just bank book entries without any realizable cash assets to pay-off urgently. This kind of generic supervision requires a deviation from the undue and popular dependence on past-based accounting data examination and verification such as capital adequacy, liquidity, impaired assets and compliance with accounting and regulatory definitions of millions of rules which provide no assurance on the current status of safety and soundness of banks or freedom from financial fraud.

- Therefore, the CB senior management must understand what it can do and can't do to serve its public duties and use scarce resources productively to deliver effectively what it can do. In that context, the proposed macroprudential authority and framework will be only a waste of time and resources.

- The dichotomy between bank regulation/supervision arm and monetary policy arm is the cause of bank problems as well as real sector problems. Unless both policies are coordinated to smoothen credit delivery mechanism across the economy, macroeconomic consequences and instabilities will affect development and living standards. This dichotomy is another fictitious hypothesis of monetarists who are unable to understand the ground reality that money, banking and economy are inseparable when the creation of money, banking business and economic activities are considered. Accordingly, the monetary policy is also a line of regulation of money and banking similar to other bank regulations that governments use to intervene in the market mechanism. Therefore, this dichotomy is like trying to separate the financial life of the economy and people between monetary policy and regulation based on bureaucratic hypotheses. As such, this is the source of most of macroeconomic and financial instabilities confronted by countries.

- Bank problems and crises that the world experiences from time to time even with all sorts of regulations and safety nets are no different from those confronted in long period of free banking up to the beginning of 20th century. Therefore, no one can provide any comfort to the public that their banking transactions are protected by modern regulations including the monetary policy. Instead, the bureaucratic cost and burden of such regulations on business innovations and market and macroeconomic efficiency are well known. However, when ever the world and countries confront banking turmoil of any sort, the first response of all governments is to tighten regulations by telling the public that the turmoil is a result of insufficient regulations and, not because of the fundamental inability and inefficiency of regulations.

- However, the habit of all regulators including central banks world over is always to stay with mouth open stating that the banking and financial system is strong and resilient because of good regulatory system. Even when there are individual bank distresses, they state that the system is safe and sound. This is a pure lie due to several fundamentals.

- First, bank stay in business of the public trust that banks have cash to repay their obligations or public transactions are protected by the government. Therefore, the public trust a pure myth and both reasons are unreal. Therefore, at any movement that the rumor starts spreading that certain banks confront lack funds, runs start accidentally. No governments can stop this unless they pump money to those banks and banking system until runs disappear. Instead, if governments start passing new regulations, the banking and financial system will end up in a financial pandemic.

- Second, the basis used by the regulators to state that the system is safe and sound and resilient is the past statistics of capital and liquidity calculated as per regulations. The numbers remaining well above the minimum required by regulations are the grounds for the safety and soundness of the sectors. This is a misconception. First, those are accounting numbers specially calculated for the past dates. Second, capital is not free cash available to be used in emergency. It is a long-term accounting concept. Third, liquidity is the value of assets portfolio (such as cash and government securities) that is believed to be used readily to raise fund in financial emergency situations. However, other than cash, the actual value of other assets available fast without losses is quite lower.

- Third, what keeps bank in business is the daily management of financial inflows and outflows that keeps customer trust intact. If the deficit is not managed in a sustainable manner, runs are inevitable in a matter of time. As banks operate on small amount of cash in proportion to bank assets and liabilities, mismanaged deficit is the bank killer. in the event the unsustainable deficit of a bank is known to the money market, the inter-bank lending to the bank will be cut-off immediately. If the money market is suspicious of several banks in this category, the inter-bank market will seize to operate. In that respect, the daily supply of funds or loans by central banks is the lifeline of blood to ailing banks. Therefore, the usual monetary operation of central banks is to provide funds to the banking system so that bank financial flows are managed without distresses and turmoil. However, central banks also unable to print money in the event of contagious bank crises as bank deposit base is huge as compared to cash available in banks because deposits are liabilities created by bank lending in book entries. Therefore, crises are inherent in banking business. But, they continue in business as called as safe and sound by central banks because bank customers are not aware of this inherent risk.

- Therefore, regulations should be treated and practiced as an intelligence-based art rather than an accounting science as believed by regulators and central banks. In that respect, the development of an AI bank regulator that operates on certain benchmarks/ guidelines stipulated by human regulators will be immensely useful in modern electronic and online era of money and banking operating on huge volume of regulations, business policies, internal controls, accounting rules and accounting statistics that human regulators have no means to assess the safety and soundness of each bank. The AI regulator will detect risks in split seconds from the bank accounting system and many banks will be closed down automatically. Otherwise, human regulators can do only the police job after each and every bank crisis by arresting and punishing those who managed banks in fraudulent manner. However, the failure of respective regulators is never resolved.

- In view of the global literature, financial stability is a hypothesis that nobody can define and supply. What countries and societies require in modern economies is a fair system of distribution of finance created with different risks in order to mobilize productive resources and improve living standards. However, many developing countries struggle in poverty and currency crises because of still primitive stages of financial systems largely owned, shared and benefitted by few business leaders and groups detrimental to the majority of the public. This is the fundamental economic and social problem confronted by these countries.

- Therefore, what country financial authorities should do is not to waste time and resources on fancy failing macroprudential/financial stability frameworks but to promote a system of the financial distribution through a wide range of products and risks (financial bio-diversity) that can reach the wider public to improve living standards. Without a policy thrust for such a wider financial system, political stories painted by party politicians for future development, prosperity and stability after decades of independence with staggering poverty are no doubt meaningless as they don't state how they find financing for all these ambitious stories. Therefore, Sri Lankan public and elected members should assess whether the country has a central bank, the nuclear of the financial distribution system, to spearhead the required financial biodiversity policy framework. However, touching the deep bureaucracy of institutions is no easy for elected members of the public due to the global network of such institutions led by IMF/World Bank. The best instance is the collapse of Liz Truss government in the UK in 45 days at the end of 2022 due to the protest staged by the Treasury, the Bank of England and the Office for Budget Responsibility (all three are independent each other) against the tax cut and growth-based mini-budget presented by Liz Truss government.

- The review of contents in the pamphlet and new legal provisions on macroprudential authority shows a grave risk of judicial actions against macroprudential professionals in the CB in the event any form of banking/financial crisis touches down in the future. The reason is the clear public mandate given to them to prevent and control systemic risks. As per legal provisions, the Minister of Finance or government is free from this responsibility and, therefore, macroprudential professionals cannot pass the blame to elected members in the event of judicial investigations.

P Samarasiri

Former Deputy Governor, Central Bank of Sri Lanka

Comments

Post a Comment