Public debt again to be a monetary policy instrument. Fiscal autonomy lost? How ethical is it?

Article's background

- The purpose of this article is to reveal a questionable provision of the brand new Public Debt Management Act certified on 18th June, 2024, i.e., section 14 that provides for public debt to serve as a monetary policy instrument for the autonomous Central Bank (CB).

- This is a strange provision in view of the brand new Central Bank of Sri Lanka Act certified on 14th September, 2023, which gave the full autonomy (operational and financial) to the CB. The autonomy is such that the CB is prohibited from even lending to the government directly or indirectly or to bailout (lender of last resort) banks in liquidity crises.

Section 14

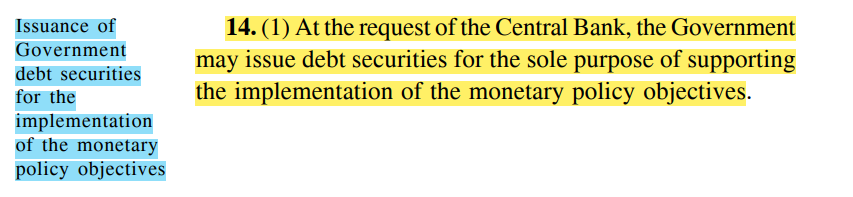

The section 14 is reproduced below.

Highlights of the section 14

- Government debt securities to be issued at the request of the CB to support the monetary policy objectives in terms of the CB Act.

- Proceeds of such securities to be deposited in a segregated account at the CB.

- The cost to be fully reimbursed by the CB.

- Outstanding amount to be reported in the govt. debt stock.

- Memorandum of understanding between the Minister and the CB in terms of the CB Act.

My comments

- It is difficulty to understand why the CB operating like monetary divine with immune instruments needs public debt to support the monetary policy.

- The new Central Bank Act is to fully separate the CB from the influence of the government and fiscal operations/debt for the CB's monetary policy and financial autonomy to ensure the domestic price stability and financial system stability entirely to the CB. Therefore, the CB to use govt debt instruments to carry out monetary policy is a serious contravention of the CB autonomy.

- This debt issuance facility is to be used as and when the CB wishes to reduce the money stock at the hand of the public directly and rapidly to control prices in general which is the purpose of the monetary policy.

- For example, if the CB wants to reduce the money stock by Rs. 200 bn during the week for a period of one year, the government can conduct an auction of one year government securities of the said amount.

- As a result, on the settlement day (i.e., two days later), currency and bank deposits of the same amount belonging to investors will be transferred to the reserve account of the government at the CB and will remain for one year in the CB vault out of public spending. As a result, the money stock held by the public will immediately decline by that amount. It is a very easy and simple monetary operation.

- Instead, if CB monetary policy instruments such as policy rates, statutory reserve ratio and CB securities are used, it will take longer time to affect the money stock or may not affect the money stock. The effect is not certain. In contrast, govt debt in local currency has a good confidence even in default situations.

- Therefore, this section of the new debt Act provides for the use of fiscal instruments for the monetary policy legally independent for the CB. It is the modern monetary theory that advocates the use of fiscal instruments to conduct the monetary policy for national objectives. Therefore, this provision seems to be secretly accepting the concept of the modern monetary theory that is overwhelmingly opposed by central banks at open platforms. As such, this is not a drafting error, but a hiddenly planned motive of extending the dominance of the CB over the government and economy. It is layman question why a so professional, efficient and autonomous central bank needs such monetary supports from the debt-ridden government. I also do not understand why such a high flying money printer wants fiscal instruments available for the welfare of the general public to be used for the control its money printing activity.

- It is not secret that the CB has been using public debt instruments and issuance systems to control interest rates under the monetary policy. The yield curve and interest rate decisions at the auctions of government securities are the known devices. The evidence of high profile monetary experts is available that a massive scale of private placements of securities was used to control interest rates under-cover. This evidence was used to cover up massive irregularities revealed from the hidden placements system.

- The new Public Debt Act also provides for the power to the Minister and Cabinet to issue government securities on non-market based mechanisms although the stipulated mechanism is the auction and other market-based mechanisms which are considered to be competitive and transparent. I can't understand why public governments want to borrow from unpublic means.

- Another questionable provision is the continuation of primary dealers appointed by the CB as at present while new primary dealers will be appointed by the Minister with the recommendation of the CB which has no responsibilities on government securities market. This severely limits the fiscal policy independence as primary dealers are interact with the CB in the money market for monetary policy operations.

- Although a memorandum and monetary policy objectives under the Central Bank Act are referred to in the Public Debt Act, the CB Act does not have such provisions.

- Despite the new Public Debt Act, Treasury bills and bonds are being issued under existing debt laws as they have not been repealed by the new Debt Act. Therefore, the purpose of the new Debt Act to improve the debt and fiscal discipline is questionable.

Remarks

- The last government hastily passed a large number of laws under the cover of the bankruptcy and boasted of its performance citing the number of such legislations notwithstanding their poor quality. My comments highlighted above show the poor quality of new public debt law.

- I am sure that the new government claimed to be pursuing for new economic, political and cultural systems in place of old systems will have the necessary teeth to look into the above cited poor quality of the public debt law and improve the law urgently before it becomes another national catastrophe.

- I recall that the US Treasury Department provided a free of charge technical assistance with a resident consultant for public debt including a draft of a consolidated public debt law and commissioning of electronic debt trading platform (a Cabinet appointed tender board also was in place). It may be worthwhile to examine what was its outcome in view of present defaulted public debt outcome.

- It is pathetic to understand how new governments fulfill public promises for living standards by their financial hands externally tied by the CB and its autonomy.

- Governments can continue such unethical acts lawfully or unlawfully without paying attention to first principles and go home after the contract period leaving the public to suffer from accumulated evil outcomes.

(This article is released in the interest of participating in the professional dialogue to find out solutions to present economic crisis confronted by the general public consequent to the global Corona pandemic, subsequent economic disruptions and shocks both local and global and policy failures. All are personal views of the author based on his research in the subject of Economics which have no intension to personally or maliciously discredit characters of any individuals.)

P Samarasiri

Former Deputy Governor, Central Bank of Sri Lanka

(35 years of staff grade service in the Central Bank, a former Director of Bank Supervision, Assistant Governor, Secretary to the Monetary Board and Compliance Officer of the Central Bank, Former Chairman of the Sri Lanka Accounting and Auditing Standards Board and Credit Information Bureau, Former Chairman and Vice Chairman of the Institute of Bankers of Sri Lanka, Former Member of the Securities and Exchange Commission and Insurance Regulatory Commission and the Author of 13 Economics and Banking Books and a large number of articles published.)

Comments

Post a Comment